March 31, 2026

Is a Personal Injury Settlement Taxable in Florida?

Living in Florida comes with a major financial perk: no state income tax. This is great news for your paycheck, and it’s even better news when you receive a personal injury settlement. You will never owe the state of Florida a dime from your compensation, whether you live in Ocala or Leesburg. However, that doesn’t mean you’re completely in the clear. The federal government has its own set of rules, and certain parts of a settlement can be considered taxable income by the IRS. This guide explains how to benefit from Florida’s laws while preparing for federal obligations.

Key Takeaways: Personal Injury Settlement Taxes in Florida

- Most personal injury settlements for physical injuries are not taxable under federal law, thanks to IRS Section 104(a)(2).

- Florida has no state income tax, so you will never owe state taxes on any part of your settlement.

- Punitive damages, pre-judgment interest, and emotional distress damages not tied to a physical injury are taxable at the federal level.

- How your settlement is structured and allocated in the agreement directly affects your tax obligations.

- A qualified personal injury attorney can help you structure your settlement to minimize taxes legally.

Receiving a personal injury settlement can bring enormous relief after months of medical bills, lost paychecks, and pain. But once the settlement check arrives, many injury victims in Florida ask the same question: Do I have to pay taxes on this money?

Contact Injury LawStars today for a free case review or call (407) 887-4690 to discuss your personal injury claim with an experienced Florida attorney.

The short answer is that most personal injury settlements are not taxable, but certain portions can be. Understanding the difference between taxable and non-taxable settlement components can save you thousands of dollars and prevent an unwelcome surprise from the IRS.

This guide breaks down exactly which parts of a Florida personal injury settlement are taxable, which are tax-free, and what steps you can take to protect your compensation.

Understanding the Personal Injury Settlement Process

After an accident, the path to receiving compensation can feel confusing. The personal injury settlement process involves several key stages, from filing your claim to finally receiving your funds. While every case is unique, most follow a similar timeline governed by legal deadlines, negotiations, and formal agreements. Understanding these steps can help you feel more in control during a challenging time. It’s important to remember that the vast majority of personal injury cases are resolved through a settlement agreement, meaning you likely won’t have to go through a full-blown trial. This process is designed to ensure all your damages are accounted for and that you receive fair compensation for your injuries, whether you were in a average car accident settlement in Florida or a slip and fall in Ocala.

The Florida Statute of Limitations: A Critical Deadline

In Florida, you have a limited window of time to take legal action after an injury. This deadline is called the statute of limitations, and for most personal injury cases, you have two years from the date of the accident to file a lawsuit. This may sound like a lot of time, but it can pass quickly when you’re focused on recovering from your injuries. Missing this deadline is critical; if you try to file a claim after it has passed, the court will almost certainly dismiss your case, and you will lose your right to seek compensation forever. That’s why it’s so important to speak with an attorney as soon as possible to protect your rights and get the process started.

How Long Does a Personal Injury Claim Take?

One of the most common questions we hear is, “How long will my case take?” The honest answer is: it depends. A straightforward claim with clear evidence and minor injuries might settle in a few months. However, a complex case involving a commercial truck accident or severe injuries could take a year or longer. Factors that influence the timeline include the severity of your injuries, the time it takes to reach maximum medical improvement, and the insurance company’s willingness to negotiate fairly. While a faster settlement might seem appealing, the goal is to secure the full compensation you deserve, and sometimes that requires patience and strategic negotiation.

Steps in the Payout Process After an Agreement

Once your attorney and the insurance company have agreed on a settlement amount, a few final steps must be completed before the money is in your hands. This final phase is crucial for ensuring all legal and financial obligations related to your case are properly handled. It involves signing official documents and the careful management of the settlement funds by your legal team. This part of the process ensures that once you receive your money, the case is officially and permanently closed, giving you peace of mind and the resources to move forward with your life.

Signing the Release Form

After reaching a verbal agreement, the insurance company will draft a settlement and release form. This is a legally binding contract that you must sign to receive your payment. By signing it, you agree that the settlement amount is the full and final compensation for your injuries from that specific accident. In exchange for the money, you “release” the at-fault party and their insurer from all future liability. It is absolutely essential to have your attorney review this document carefully before you sign, as it permanently closes your claim.

Receiving and Distributing Funds

Once you sign the release form, the insurance company will issue the settlement check. This check is not sent directly to you; instead, it is sent to your lawyer’s office and deposited into a special trust account, often called an IOTA account. Your attorney then acts as a distributor, using those funds to pay off all the case-related expenses. This includes covering their legal fees, reimbursing case costs, and satisfying any medical liens or bills. This ensures all financial loose ends are tied up before the final net amount is disbursed to you.

How Long Until You Receive Your Money?

Patience is key during the final stage of your settlement. After a settlement amount is agreed upon, it typically takes about six weeks to receive your portion of the funds. This timeframe accounts for several steps: the insurance company needs time to draft the release form and mail it, you need time to review and sign it, and then they need to process and mail the check. Once your attorney receives the check, it must clear in their trust account. Finally, your legal team will pay any outstanding liens and fees before writing your final check. While it can feel like a long wait, this structured process ensures everything is handled correctly.

Common Reasons for Settlement Delays

While many cases proceed smoothly, some factors can cause delays. A primary reason is a dispute over liability—if the insurance company argues that their client wasn’t at fault, it can prolong negotiations. Delays can also occur if there are questions about whether your injuries were directly caused by the accident or if you had a pre-existing condition. Cases involving multiple at-fault parties or significant injuries that require long-term medical analysis can also take more time. Sometimes, insurance companies may intentionally use delay tactics, hoping you’ll get frustrated and accept a lower offer. An experienced attorney can help manage these issues and keep your case moving forward.

What is a Typical Personal Injury Settlement Amount?

There is no “typical” settlement amount because every personal injury case is different. The value of your claim depends on a unique combination of factors, including the severity of your injuries, the total cost of your medical treatment (both past and future), and the amount of income you lost from being unable to work. Another significant component is “pain and suffering,” which compensates you for the physical pain and emotional distress the accident caused. An experienced personal injury lawyer can evaluate all these elements to determine a fair value for your claim. Whether your accident occurred in The Villages, Leesburg, or anywhere in between, the specific details of your case will ultimately dictate the settlement amount you can expect to recover.

Why Most Personal Injury Cases Settle

The vast majority of personal injury cases in Florida are resolved through a settlement rather than a court trial. There are several good reasons for this. Settling a case is generally faster, less stressful, and more predictable than going to trial. A trial can be a lengthy, expensive process with an uncertain outcome, as the final decision is left in the hands of a judge or jury. A settlement, on the other hand, provides a guaranteed amount of compensation. Both sides often prefer to negotiate a resolution they can agree on, allowing them to avoid the risks and additional costs associated with litigation.

A Warning About Early Settlement Offers from Insurance Companies

Shortly after an accident, you might receive a call from the at-fault party’s insurance adjuster with a quick settlement offer. While it might be tempting to accept easy money, you should be very cautious. Insurance companies are businesses, and their goal is to pay out as little as possible. These initial offers are often “lowball” amounts that represent only a fraction of what your case is truly worth—sometimes as low as 30-40%. Adjusters hope you’ll take the offer before you understand the full extent of your injuries or speak with an attorney. Accepting an early offer means you forfeit your right to seek more compensation later, even if your medical condition worsens.

You Have the Final Say in Your Settlement

While your attorney will handle all the negotiations, the ultimate decision to accept or reject a settlement offer is always yours. A good lawyer will provide their professional recommendation based on the facts of your case, the strength of the evidence, and their experience with similar claims. They will advise you on whether an offer is fair and explain the potential risks and rewards of proceeding to trial. At Injury LawStars, we believe in empowering our clients with the information they need to make the best choice for themselves and their families. Our role is to guide and advocate for you, but you remain in control of the final decision.

How a Settlement Payout is Divided

When the settlement check arrives, it represents the total gross amount recovered for your case. However, this entire amount doesn’t go directly into your pocket. Before you receive your final payment, several deductions must be made from the total settlement. These typically include attorney’s fees, case-related costs and expenses, and any outstanding medical bills or liens. Understanding this breakdown is crucial for managing your expectations and seeing how each dollar is allocated. A transparent law firm will provide you with a detailed settlement statement that clearly itemizes all of these deductions, so you know exactly where the money is going and why.

Attorney’s Fees on a Contingency Basis

Most personal injury lawyers, including our team at Injury LawStars, work on a contingency fee basis. This arrangement is designed to help accident victims get high-quality legal representation without any upfront costs. Simply put, you don’t pay any attorney’s fees unless we win or settle your case. The fee is a pre-agreed-upon percentage of the total settlement amount. This system ensures that everyone has access to justice, regardless of their financial situation. It also means our goals are perfectly aligned with yours: we are motivated to secure the maximum possible compensation for you, because our payment is directly tied to the success of your case.

How Injury LawStars Handles Fees

At Injury LawStars, we are committed to transparency. We operate on a contingency fee basis, which means you pay us nothing unless we successfully recover money for you. Before we even begin working on your case, we will explain our fee structure clearly, so there are no surprises down the road. Our fee is calculated as a percentage of the gross settlement amount, before any costs or medical bills are deducted. This approach ensures our interests are directly aligned with yours—the more we can recover for you, the better the outcome for everyone involved. We believe this is the fairest way to help injury victims in communities like Wildwood, Bushnell, and across Florida.

Covering Case Costs and Expenses

Beyond attorney’s fees, every lawsuit involves certain operational costs. These are the out-of-pocket expenses your law firm pays to build and pursue your case effectively. Common examples include court filing fees, the cost of obtaining medical records and police reports, deposition transcription fees, and fees for expert witnesses, such as accident reconstructionists or medical specialists. Reputable firms like ours will advance these costs on your behalf, so you don’t have to pay for anything while your case is ongoing. These expenses are then reimbursed from the total settlement amount after the attorney’s fees are calculated.

Paying Medical Bills and Liens

After an accident, you likely have a stack of medical bills from hospitals, doctors, and physical therapists. If your health insurance paid for some of your treatment, they may have a right to be reimbursed from your settlement—this is called a subrogation claim. Similarly, if a provider treated you under a “letter of protection,” they have a legal claim, or lien, on your settlement funds. All of these medical liens must be paid from the settlement proceeds before you can receive your share. This step is legally required to ensure your medical providers are compensated for the care they provided you.

How a Lawyer Can Negotiate Your Medical Bills

One of the most valuable services a personal injury attorney provides is negotiating your medical liens. We don’t just accept the initial bills from hospitals or insurance companies. Instead, we contact each provider and work to reduce the amount you owe. Because we handle these negotiations regularly, we can often secure significant reductions. For example, we might be able to negotiate a $20,000 hospital lien down to $12,000. Every dollar we save you on medical bills is another dollar that goes directly into your pocket, maximizing your net recovery.

Example of a $100,000 Settlement Breakdown

To see how this works in practice, let’s imagine a $100,000 settlement. First, the attorney’s fee, typically one-third (33.3%), would be $33,333. Next, let’s say the case costs totaled $5,000. That leaves $61,667. From this amount, we would pay your medical liens. If your original medical bills were $30,000, but your attorney negotiated them down to $20,000, that amount would be paid to the providers. The remaining $41,667 would be your net, take-home amount. As this example shows, a skilled attorney can significantly increase your final payout by effectively negotiating your medical debts.

What if a Fair Settlement Can’t Be Reached?

While most personal injury claims are resolved through settlement negotiations, there are times when the insurance company simply refuses to make a fair offer. When you and your attorney believe your claim is worth more than the insurer is willing to pay, you aren’t out of options. At this point, the case may proceed toward litigation. However, before going to a full trial, there are often intermediate steps known as alternative dispute resolution (ADR). These methods, such as mediation and arbitration, are designed to help both sides reach an agreement without the time and expense of a courtroom battle. They provide a structured environment to resolve disagreements and find a middle ground.

Mediation

Mediation is a common step in personal injury cases, especially after a lawsuit has been filed. It is a confidential process where you, your attorney, the insurance adjuster, and their lawyer meet with a neutral third-party called a mediator. The mediator’s job is not to make a decision but to facilitate a productive conversation between the two sides. They will go back and forth between the parties, discussing the strengths and weaknesses of the case and exploring potential compromises. The goal is to help everyone reach a mutually agreeable settlement. If an agreement is reached, it becomes legally binding; if not, you can still proceed to trial.

Arbitration

Arbitration is another form of ADR, but it is more formal than mediation and functions like a simplified, private trial. In arbitration, both sides present their case to a neutral arbitrator (or a panel of arbitrators), who acts like a judge. They will listen to the evidence and arguments from both parties and then make a decision on the outcome of the case. Depending on what was agreed to beforehand, the arbitrator’s decision can be either binding or non-binding. A binding decision is final and legally enforceable, much like a court verdict, while a non-binding decision serves as a recommendation that the parties can choose to accept or reject.

Why Is a Personal Injury Settlement Taxed Differently?

Under normal circumstances, the IRS considers virtually all income taxable. Wages, investment returns, freelance income, and even prizes are all subject to federal income tax. So why are personal injury settlements treated differently?

The answer lies in the purpose of the payment. A personal injury settlement is designed to make you whole after someone else’s negligence caused you harm. It replaces what you lost, whether that means covering medical expenses, compensating for physical pain, or restoring income you could not earn while recovering. Congress recognized that taxing money meant to restore an injured person to their pre-accident condition would be unfair, which is why specific tax exclusions exist.

However, not every dollar in a settlement serves a purely compensatory purpose. Some components, like punitive damages or interest on delayed payments — often most common in wrongful death settlement cases — go beyond restoring what was lost. The IRS treats these differently, and understanding where the line falls is critical for anyone receiving a personal injury settlement in Florida.

The IRS Rule That Protects Your Settlement: Section 104(a)(2)

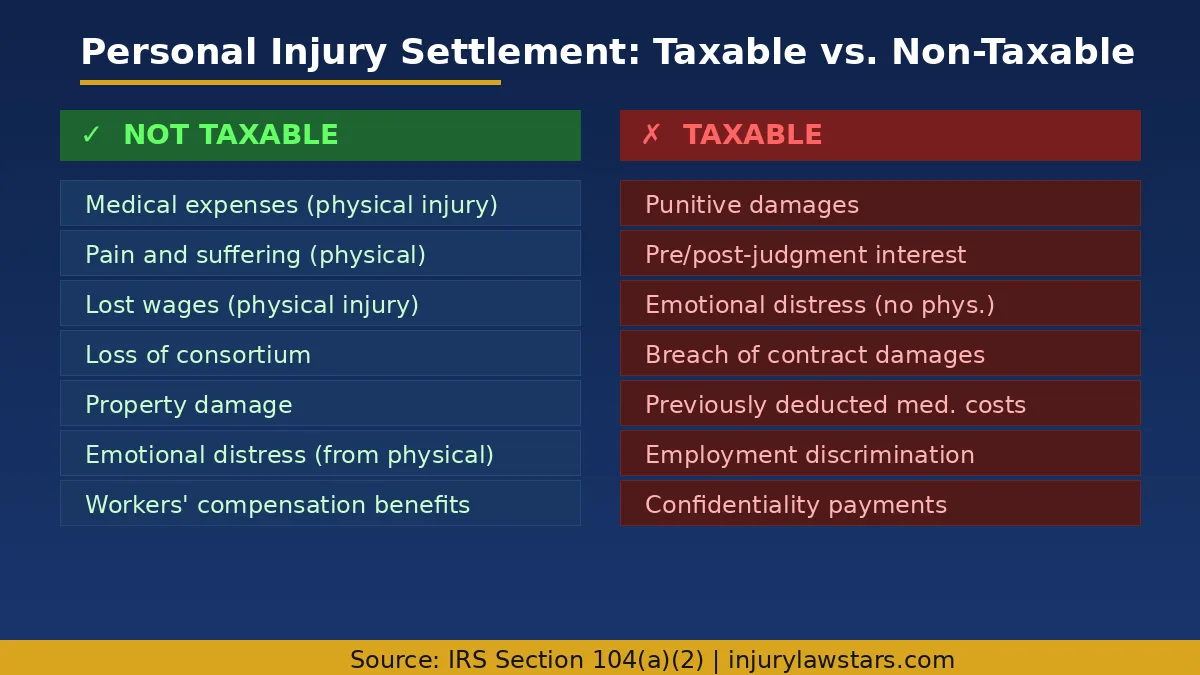

The federal tax code provision that governs personal injury settlement taxation is Internal Revenue Code Section 104(a)(2). This section states that damages received “on account of personal physical injuries or physical sickness” are excluded from gross income. This exclusion applies whether you receive the money through a court judgment or a negotiated settlement, and whether it arrives as a lump sum or periodic payments.

For the exclusion to apply, two conditions must be met:

- The claim must involve a physical injury or physical sickness. Purely emotional or psychological claims without a physical component do not qualify for the exclusion.

- The damages must be compensatory, not punitive. Section 104(a)(2) specifically excludes punitive damages from the tax exemption.

This means that if you were injured in a car accident, truck accident, slip and fall, or any other incident that caused physical harm, the compensation you receive for that physical injury is generally tax-free at the federal level.

Which Parts of Your Settlement Are Tax-Free?

The following categories of damages are typically excluded from federal income tax when they stem from a physical injury or physical sickness:

Payments for Your Medical Bills

Compensation for past and future medical bills related to your physical injury is not taxable. This includes emergency room visits, surgeries, physical therapy, prescription medications, rehabilitation, and any ongoing medical care tied to your injuries. However, there is one important exception: if you previously deducted medical expenses on your tax return and then receive settlement money reimbursing those same expenses, you may need to report that reimbursed amount as income. This is known as the medical expense deduction recapture rule.

Damages for Pain and Suffering

Compensation for pain and suffering connected to a physical injury is not taxable. This covers both the physical discomfort and the emotional distress that results directly from your physical injuries. The key requirement is that the pain and suffering must be linked to a physical injury, not a standalone emotional claim.

Income You Lost Due to Injury

When lost wages are included as part of a physical injury settlement, they are generally not taxable under Section 104(a)(2). This may seem counterintuitive since wages are normally taxable income, but the IRS recognizes that lost wage compensation in a physical injury case is fundamentally different from employment income. It replaces earnings you could not make because of your physical injuries.

Compensation for Loss of Consortium

Damages paid to a spouse for loss of companionship, affection, or marital relations caused by the injured person’s physical injuries are generally not taxable, provided they originate from a physical injury claim.

Reimbursement for Property Damage

Compensation for damaged or destroyed property, such as vehicle repair or replacement costs after a car accident, is generally not taxable as long as the payment does not exceed the property’s adjusted basis (essentially, what you paid for it). If the settlement exceeds the adjusted basis, the excess may be considered taxable gain.

Which Parts of Your Settlement Might Be Taxable?

Understanding the types of damages in your case matters here, because the IRS treats economic and non-economic damages differently from punitive damages.

While the majority of a physical injury settlement is typically tax-free, several categories of damages are subject to federal income tax regardless of whether the underlying case involves a physical injury:

Are Punitive Damages Taxable?

Yes. Punitive damages are always taxable under federal law. Unlike compensatory damages that reimburse your losses, punitive damages are awarded to punish the defendant for egregious behavior. Because they are not compensating you for a loss, the IRS treats them as taxable income. This applies even when punitive damages are awarded alongside a physical injury claim.

There is one narrow exception: in states where the wrongful death statute allows only punitive damages, those damages may be excluded. Florida’s wrongful death law allows compensatory damages, so this exception generally does not apply in Florida cases.

Is Interest on a Settlement Taxable?

Yes. Pre-judgment and post-judgment interest added to your settlement or court award is taxable income. Interest accrues when there is a delay between the injury and the payment, and the IRS considers this interest income regardless of the underlying claim type.

When Emotional Distress Damages Are Taxed

If you receive compensation for emotional distress that does not originate from a physical injury or physical sickness, that amount is taxable. For example, if you filed a claim for workplace harassment that caused anxiety and depression but no physical injury, the damages for emotional distress would be subject to federal income tax. However, you can reduce the taxable amount by the cost of medical treatment for the emotional distress (such as therapy or counseling costs).

Taxes on Non-Physical Injury Claims

Settlements for breach of contract, employment discrimination (without physical injury), defamation, or other non-physical injury claims are generally taxable because they do not fall under the Section 104(a)(2) exclusion.

What Florida’s No-Income-Tax Rule Means for Your Settlement

Florida is one of the few states in the country that does not impose a personal income tax. This provides a significant advantage for personal injury settlement recipients compared to residents of states like California, New York, or Illinois where state income tax rates can reach 10% or higher.

Here is what Florida’s tax structure means for your settlement:

- No state taxes on any part of your settlement. Whether your settlement includes compensatory damages, punitive damages, or interest, Florida will not tax any portion at the state level.

- Federal tax rules still apply. Even though Florida does not impose state income tax, you must still follow IRS rules for reporting and paying federal taxes on taxable settlement components.

- Potential savings on taxable components. If your settlement includes punitive damages or interest, you will only owe federal income tax on those amounts. In a state with income tax, you would owe both federal and state taxes, making Florida a more favorable place to receive a settlement.

If you have been injured in Florida and need help maximizing your settlement, reach out to Injury LawStars or call (407) 887-4690 for a free consultation.

Strategies to Legally Minimize Taxes on Your Settlement

While you cannot entirely eliminate federal taxes on inherently taxable settlement components, there are several legal strategies that can help minimize your tax burden:

Strategically Allocating Your Settlement Funds

How your settlement is allocated in the settlement agreement matters enormously. The agreement should clearly specify which portions compensate for physical injuries, medical expenses, lost wages tied to physical injury, pain and suffering, and other categories. Vague or improperly allocated settlements can lead to the IRS treating ambiguous amounts as taxable income. Work with your attorney to ensure the settlement language precisely reflects the nature of each payment.

Considering a Structured Settlement

A structured settlement spreads your compensation over time through periodic payments rather than a single lump sum. Structured settlements can offer significant tax advantages:

- The full amount, including any growth or interest earned within the structured settlement, remains tax-free if the underlying damages are for physical injury.

- Periodic payments can help you manage your finances over time and avoid spending a large lump sum too quickly.

- Investment gains within a structured settlement are not taxed, unlike gains you might earn if you invested a lump sum on your own.

Structured settlements are especially valuable for large settlements or for individuals who want guaranteed, long-term income.

Lump-Sum Payments: Pros and Cons

A lump-sum payment means you receive your entire settlement at once. The biggest advantage is immediate access to your funds. This can be crucial if you have piled up medical bills or have been out of work and need to cover living expenses right away in places like Ocala or The Villages. Having the full amount gives you complete control to pay off debts, make large purchases, or invest the money as you see fit. However, this control comes with risks. Receiving a large amount of money can be overwhelming, and without careful financial planning, it’s easy to overspend or make poor investment choices, potentially leaving you without funds for future needs.

Structured Payments: Pros and Cons

A structured settlement provides your compensation through a series of guaranteed payments over time instead of all at once. The primary benefit is long-term financial security. This approach ensures you have a steady, reliable income stream to cover ongoing medical care or replace lost future earnings, which is especially important in cases involving catastrophic injuries like a brain injury settlement case. It also protects the settlement from being spent too quickly. The main drawback is the lack of flexibility. You won’t have immediate access to the full settlement amount, which could be a problem if a large, unexpected expense comes up. Deciding between a lump sum and a structured settlement depends entirely on your personal financial situation and long-term needs.

Clearly Separating Your Claims

If your case involves both physical injury claims and non-physical claims (such as a separate breach of contract or employment dispute), your attorney can negotiate to allocate more of the settlement toward the physical injury components, which are tax-free. This must be done honestly and reflect the actual nature of the damages, but proper allocation is a legitimate and commonly used strategy.

Document Everything

Keep thorough records of all medical treatments, out-of-pocket expenses, and communications related to your injury. Strong documentation supports the categorization of your settlement as compensation for physical injuries and helps defend the tax-free treatment of your settlement if the IRS ever questions it.

Do You Need to Report Your Settlement to the IRS?

Even if your entire settlement is non-taxable, you may still need to be aware of IRS reporting requirements:

- Form 1099-MISC: If the payer (typically the insurance company or defendant) considers any portion of your settlement taxable, they may issue a Form 1099-MISC reporting the payment. You will need to address this on your tax return, even if you believe the amount is excludable under Section 104(a)(2).

- No 1099 for non-taxable amounts: If your entire settlement is for physical injuries and is non-taxable, the payer generally will not issue a 1099. However, it is wise to keep your settlement agreement and attorney correspondence as documentation.

- Attorney fees: If you paid your attorney on a contingency fee basis (which is standard in personal injury cases), the tax treatment of attorney fees depends on the underlying claim. For physical injury settlements excluded under Section 104(a)(2), the attorney’s share is typically not reported as your income.

Common Tax Mistakes to Avoid With Your Settlement

Settlement recipients frequently make errors that create unnecessary tax liability. Here are the most common mistakes to avoid:

- Failing to allocate the settlement properly. If your settlement agreement does not specify what each payment covers, the IRS may treat the entire amount as taxable. Always insist on clear allocation language.

- Forgetting about the medical expense deduction recapture. If you deducted medical expenses in a prior year and your settlement reimburses those same expenses, you must report the reimbursed amount as income.

- Ignoring interest. Interest on a settlement is taxable even when the underlying damages are not. Many recipients overlook interest income and fail to report it.

- Not consulting a tax professional. Personal injury settlement taxation can be complex, especially when your settlement includes multiple damage categories. A tax advisor who understands settlement taxation can help you plan effectively and avoid costly mistakes.

- Spending the settlement without reserving funds for taxes. If any portion of your settlement is taxable, set aside enough to cover the federal tax liability before spending the rest. Failing to do so can result in penalties and interest from the IRS.

When Should You Talk to a Tax Professional?

While many straightforward physical injury settlements do not require specialized tax advice, you should consult a tax professional or CPA if:

- Your settlement includes punitive damages or interest.

- Your settlement involves both physical and non-physical injury claims.

- You previously deducted medical expenses that your settlement now reimburses.

- Your settlement is large enough to significantly affect your overall tax bracket.

- You are considering a structured settlement and want to understand the long-term tax implications.

- You received a Form 1099-MISC for amounts you believe are non-taxable.

A qualified tax professional can help ensure you comply with federal requirements while keeping as much of your settlement as possible.

Need an experienced Florida personal injury attorney who understands how to protect your settlement? Contact Injury LawStars or call (407) 887-4690 for a free consultation today.

Frequently Asked Questions About Personal Injury Settlement Taxes

Are personal injury settlements taxable in Florida?

Most personal injury settlements for physical injuries are not taxable at the federal level under IRS Section 104(a)(2), and Florida has no state income tax. However, punitive damages, pre-judgment interest, and emotional distress damages not connected to a physical injury are taxable under federal law.

Do you have to pay taxes on a settlement for a car accident?

Generally no, if the settlement compensates you for physical injuries from the car accident. Compensation for medical bills, pain and suffering, and lost wages tied to your physical injuries is typically tax-free. Punitive damages or interest would be taxable.

How can I avoid paying taxes on settlement money?

Ensure your settlement agreement clearly allocates payments to physical injury categories, consider a structured settlement for large awards, keep detailed documentation of your injuries and medical treatment, and work with both a personal injury attorney and a tax professional to structure your settlement favorably.

Are lost wages from a personal injury settlement taxable?

Lost wages included in a physical injury settlement are generally not taxable under Section 104(a)(2). However, if the lost wages are part of a non-physical injury claim (such as employment discrimination without physical injury), they would be taxable.

Is workers’ compensation taxable in Florida?

No. Workers’ compensation benefits are generally not taxable at either the federal or state level, provided you do not also receive Social Security disability benefits. If you receive both, a portion of your workers’ compensation may become taxable.

What happens if I get a 1099 for my settlement?

If you receive a Form 1099-MISC, you should report it on your tax return but may be able to exclude the amount from taxable income if the settlement qualifies under Section 104(a)(2). Consult a tax professional to properly handle the reporting and claim the exclusion.

Related Articles

- Do I Have to Pay Medical Bills from My Settlement?

- Injury LawStars | Florida Personal Injury Lawyer

- Injury LawStars | Orlando Personal Injury Lawyer

About the Author

Katie Miller, Esq.

Managing Partner · Injury LawStars

Attorney Katie Miller was once an injury victim herself. After a car accident in 2016 that required spinal surgery and a 13-month recovery, she turned her experience into a mission: fighting for people who are hurting. With 17+ years of legal experience and over \$45 million recovered for clients, Katie brings both professional expertise and personal understanding to every case.