May 14, 2026

Florida PIP Insurance After an Accident: What to Know

Florida PIP Insurance After an Accident: What to Know

Key takeaway: Florida PIP insurance after an accident is usually your first source of medical bill and wage-loss coverage, no matter who caused the crash. But PIP has strict limits. You generally must get medical treatment within 14 days, it pays only a percentage of covered losses, and many serious injuries quickly exceed the available benefits.

After a crash, the questions come fast. Who pays the emergency room bill? Should you call your own insurance company or the other driver’s insurer? What happens if the adjuster says you waited too long to see a doctor? Florida’s no-fault system is supposed to make initial benefits easier to access, but in practice it can feel confusing, rushed, and stacked in favor of insurance companies.

This guide explains how PIP works in Florida, what it may cover, what it does not cover, the 14-day treatment rule, when you may be able to pursue a claim beyond no-fault benefits, and the steps you can take now to protect your rights.

What Is PIP Insurance in Florida?

PIP stands for Personal Injury Protection. It is the part of a Florida auto insurance policy that can pay certain medical expenses, lost wages, and related benefits after a motor vehicle accident. Florida is commonly called a no-fault state because your own PIP coverage usually pays first, regardless of who caused the crash.

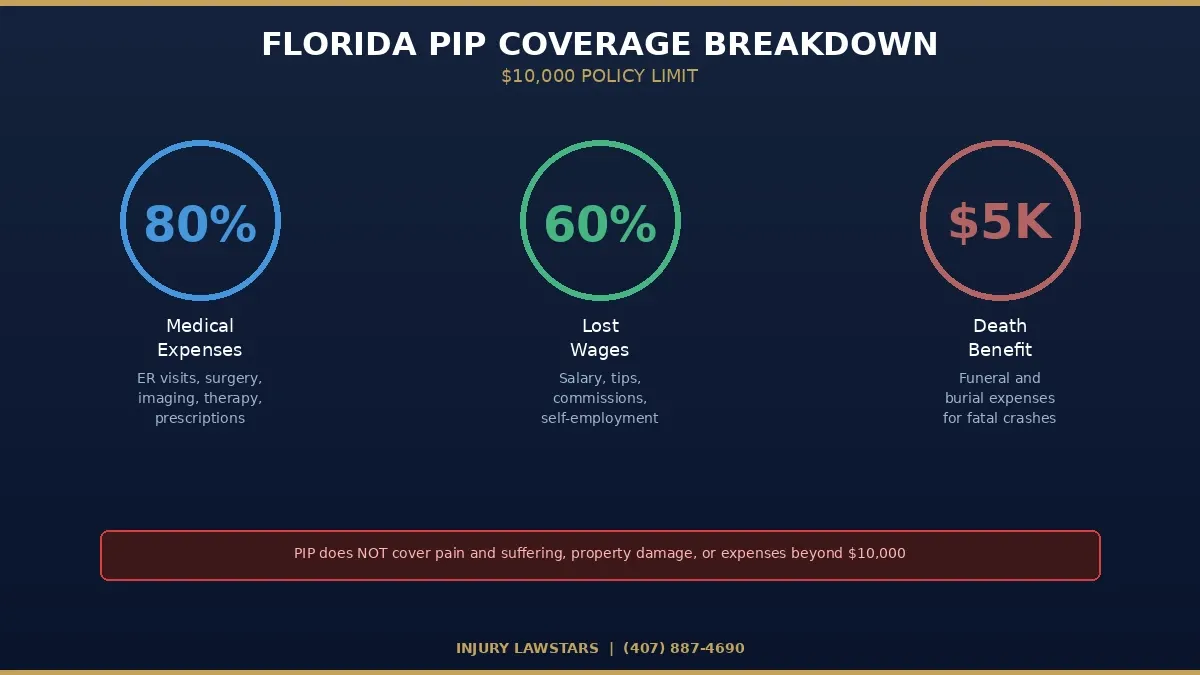

Florida law generally requires owners of registered vehicles with four or more wheels to carry at least $10,000 in PIP coverage and $10,000 in property damage liability coverage. The PIP rules are found primarily in Florida Statute 627.736.

That does not mean fault is irrelevant. Fault still matters for vehicle damage, serious injury claims, liability disputes, and compensation that goes beyond PIP. The no-fault system simply means your own insurer is usually the first place you turn for injury-related benefits after a car accident.

How Does PIP Work in Florida After a Car Accident?

In a typical Florida crash, PIP works in a sequence:

- You get medical care. This should happen as soon as possible, and generally within 14 days, to protect PIP eligibility.

- You notify your auto insurer. Your own PIP carrier opens a claim for accident-related medical expenses and wage loss.

- Medical providers bill PIP. The insurer reviews whether the treatment is related, reasonable, necessary, and documented.

- PIP pays up to policy limits. Minimum PIP coverage is $10,000, but available benefits may be lower if there is no qualifying Emergency Medical Condition diagnosis.

- You evaluate whether the case goes beyond PIP. If injuries are serious, permanent, or otherwise meet Florida’s threshold, you may have a claim against the at-fault driver.

For many injured people, the most surprising part is that your own insurer may become the company questioning your treatment, requesting records, scheduling exams, and looking for reasons to limit payment. That is why documentation matters from day one.

What Does Florida PIP Cover?

Florida PIP may cover several categories of loss, subject to the policy language, statutory rules, deductibles, exclusions, and available limits.

Medical expenses

PIP generally pays 80% of reasonable, necessary, and accident-related medical expenses up to the available policy limit. Covered treatment may include:

- Ambulance transportation

- Emergency room treatment

- Hospital care

- Doctor visits

- Diagnostic imaging such as X-rays, CT scans, and MRIs

- Prescription medications

- Physical therapy and rehabilitation

- Specialist evaluations

- Some chiropractic care, depending on the circumstances and documentation

Lost income

If crash injuries prevent you from working, PIP may pay 60% of covered lost wages, again subject to available limits. Wage-loss documentation is important. You may need employer verification, pay records, medical work restrictions, and proof that the accident injuries caused the missed work.

Replacement services

PIP may also cover a percentage of replacement services for tasks you normally performed but cannot do because of your injuries. This can include certain household duties or other necessary services, depending on the facts.

Death benefits

If a covered crash causes death, PIP may provide a death benefit, often described as $5,000 under Florida law, in addition to other potential wrongful death rights. If your family is facing this situation, speak with a Florida wrongful death attorney before signing insurance paperwork.

What PIP Does Not Cover

PIP is helpful, but it is not full compensation for a serious car accident. In many cases, PIP does not cover:

- All medical bills. PIP usually pays only 80% of covered medical expenses, and only up to the available limit.

- All lost income. PIP generally pays 60% of covered wage loss, not 100%.

- Pain and suffering. PIP does not compensate you for physical pain, emotional distress, loss of enjoyment of life, or inconvenience.

- Vehicle damage. Property damage is handled separately, often through the at-fault driver’s property damage liability coverage or your own collision coverage.

- Future losses beyond the limit. Once PIP is exhausted, it does not keep paying for ongoing care.

- Every disputed treatment bill. Insurers may deny treatment they claim is unrelated, unreasonable, unnecessary, late, or poorly documented.

This is where many crash victims get caught. A $10,000 PIP limit can sound like meaningful protection until you have an ambulance bill, emergency room bill, imaging, follow-up visits, and weeks of missed work. The coverage can disappear quickly.

The 14-Day Rule for Florida PIP Claims

One of the most important rules for Florida PIP insurance after an accident is the 14-day medical treatment requirement. In general, you must seek initial medical care within 14 days of the crash to preserve PIP benefits.

If you wait longer than 14 days to get medical care, the insurance company may deny PIP benefits entirely.

This rule is especially dangerous because many injuries do not feel severe right away. Adrenaline can mask pain. A sore neck may become radiating arm pain. A headache may become concussion symptoms. Back pain may worsen after swelling increases. Waiting to see whether symptoms improve can give the insurer an argument that your injuries are not covered.

Who can provide initial treatment?

Qualifying treatment can involve providers such as physicians, hospitals, emergency medical providers, dentists for dental injuries, physician assistants, and advanced practice registered nurses. The details matter, so do not assume that every provider visit satisfies every PIP requirement.

What is an Emergency Medical Condition?

An Emergency Medical Condition, often called an EMC, is another critical PIP issue. If a qualified medical provider determines that your injury qualifies as an EMC, you may be eligible for the full $10,000 in PIP benefits. Without an EMC determination, available PIP benefits may be limited to $2,500.

That difference can matter immediately. A $2,500 cap may not cover an emergency room visit and initial imaging. Prompt medical evaluation and clear documentation can help protect the benefits available to you.

Car Accident Medical Bills in Florida: Who Pays First?

For many injured drivers and passengers, the practical question is simple: who pays the bills?

In many Florida car accident cases, the payment order may look like this:

- PIP pays first for covered medical bills and wage loss, subject to percentages and limits.

- Health insurance may become involved after PIP is exhausted or for bills not handled by PIP.

- Medical providers may assert balances or liens depending on billing arrangements and coverage.

- The at-fault driver’s insurer may be responsible if your injuries meet Florida’s serious injury threshold or if another legal basis supports a claim.

- Uninsured or underinsured motorist coverage may apply if the at-fault driver has no insurance or not enough insurance.

These layers can create confusion, especially when providers, insurers, and adjusters all send letters at the same time. A Florida car accident lawyer can help organize coverage, protect deadlines, and pursue compensation beyond PIP when the facts support it.

When Can You Step Outside Florida No-Fault and Sue?

Florida’s no-fault system limits some claims, but it does not prevent every lawsuit. If your injuries meet the serious injury threshold, you may be able to pursue compensation from the at-fault driver for losses PIP does not cover.

Under Florida Statute 627.737, qualifying injuries can include:

- Significant and permanent loss of an important bodily function

- Permanent injury within a reasonable degree of medical probability

- Significant and permanent scarring or disfigurement

- Death

Examples may include serious back and neck injuries, traumatic brain injuries, fractures with lasting limitations, permanent scarring, internal injuries, and other conditions that substantially affect your life. If you suffered a head injury, learn more about Florida brain injury claims and why early documentation matters.

Common Insurance Company Tactics After a PIP Claim

Insurance companies know the PIP rules well. They also know that most injured people do not. Watch for tactics such as:

- Using delay against you. The adjuster may argue that late treatment means your injuries are unrelated or not serious.

- Requesting recorded statements early. A statement given while you are in pain, medicated, or confused may later be used to challenge the claim.

- Disputing medical necessity. Insurers may claim therapy, imaging, specialist care, or ongoing treatment is excessive.

- Pointing to prior conditions. If you had an old back, neck, or shoulder issue, the insurer may blame that instead of the crash.

- Scheduling an insurance medical exam. The insurer’s chosen doctor may minimize your injuries or recommend cutting off benefits.

- Offering a quick settlement. Early offers may arrive before you know the full extent of your injuries, future care needs, or wage loss.

You do not have to navigate these tactics alone. Attorney Katie Miller founded Injury LawStars with a personal understanding of what injury victims face. After surviving a serious crash herself, she knows how overwhelming the process can be when you are trying to heal and protect your future at the same time.

Step-by-Step Checklist After a Florida Car Accident

Use this checklist to protect your health, your PIP benefits, and any claim beyond PIP:

- Call 911 if anyone may be hurt. Get emergency help and create an official record.

- Report the crash. A police report can help document location, drivers, vehicles, witnesses, and initial fault details.

- Get medical care immediately. Do not wait. Protect the 14-day PIP deadline and your health.

- Tell doctors every symptom. Mention neck pain, back pain, headaches, numbness, dizziness, anxiety, sleep issues, and any other changes.

- Photograph everything. Take pictures of vehicles, injuries, road conditions, skid marks, debris, insurance cards, and the crash scene.

- Save all paperwork. Keep bills, discharge instructions, prescriptions, work notes, claim letters, and repair estimates.

- Notify your insurer, but be careful. Provide required notice, but avoid guessing about fault, injuries, or long-term recovery.

- Do not accept a fast settlement without advice. Once you sign a release, you may lose the right to seek more compensation.

- Contact an attorney early. Legal guidance can help protect PIP, identify additional coverage, and stop adjusters from taking advantage of you.

How Injury LawStars Helps Protect PIP and Injury Claims

Injury LawStars represents accident victims throughout Florida, including Clermont, Orlando, Ocala, The Villages, Tampa, Jacksonville, Kissimmee, Lakeland, and surrounding communities. The firm handles cases involving car crashes, truck accidents, motorcycle crashes, pedestrian injuries, bicycle accidents, and other serious injury claims.

When we help with a crash claim, we look beyond the first PIP payment. Our team can help:

- Identify all available insurance coverage

- Protect the 14-day treatment rule and other deadlines

- Collect medical records, bills, wage records, and crash evidence

- Address improper PIP denials or benefit reductions

- Evaluate whether injuries meet the serious injury threshold

- Negotiate with insurance companies

- Pursue compensation for damages beyond PIP when the law allows

Frequently Asked Questions About Florida PIP Insurance

How does PIP work in Florida after an accident?

PIP usually pays first through your own auto insurance policy, regardless of who caused the crash. It may cover 80% of reasonable accident-related medical expenses and 60% of covered lost wages, up to available policy limits. Minimum required PIP coverage is generally $10,000.

What is the 14-day rule for Florida PIP?

The 14-day rule generally requires you to seek initial medical treatment within 14 days of the accident to qualify for PIP benefits. If you wait too long, your insurer may deny benefits even if your injuries are real and crash-related.

Does PIP pay all car accident medical bills in Florida?

No. PIP usually pays only a percentage of covered bills and only up to the available limit. It also does not cover pain and suffering. Serious injuries may require a claim beyond PIP against the at-fault driver or another available insurance policy.

Can I sue the other driver if Florida is a no-fault state?

Yes, if your injuries meet Florida’s serious injury threshold or another legal basis applies. Serious injuries may include permanent injury, significant and permanent loss of an important bodily function, significant scarring or disfigurement, or death.

What if my PIP benefits are denied?

A denial does not always mean the insurer is right. The company may be disputing treatment timing, medical necessity, documentation, or the relationship between the crash and your injuries. An attorney can review the denial and explain your options.

Does PIP cover motorcycle accidents in Florida?

Florida’s PIP requirement generally applies to motor vehicles with four or more wheels, not motorcycles. If you were hurt on a motorcycle, speak with a Florida motorcycle accident lawyer about other insurance coverage and injury claim options.

Should I talk to the insurance adjuster after a crash?

You may need to notify your insurer, but be careful with recorded statements, broad medical authorizations, and questions that ask you to guess. Before giving detailed statements or accepting money, consider getting legal advice.

Get Help With a Florida PIP Claim After an Accident

Florida PIP insurance can help with immediate medical bills, but it is not enough for many injured people. The deadlines are strict, the benefits are limited, and insurance companies often look for ways to reduce what they pay.

If you were hurt in a crash, Injury LawStars can help you understand what PIP may cover, whether you may have a claim beyond no-fault benefits, and how to protect your recovery from the start.

Call Injury LawStars today for a free consultation. No upfront fees. No hourly fees. No fees unless we win.

This article is for general informational purposes only and is not legal advice. Every case is different. Speaking with an attorney about your specific facts is the best way to understand your rights.

About the Author

Katie Miller, Esq.

Managing Partner · Injury LawStars

Attorney Katie Miller was once an injury victim herself. After a car accident in 2016 that required spinal surgery and a 13-month recovery, she turned her experience into a mission: fighting for people who are hurting. With 17+ years of legal experience and over \$45 million recovered for clients, Katie brings both professional expertise and personal understanding to every case.