March 31, 2026

Are Personal Injury Settlements Taxable in Florida?

Key Takeaways: Personal Injury Settlement Taxes in Florida

- Most personal injury settlements for physical injuries are not taxable under federal law, thanks to IRS Section 104(a)(2).

- Florida has no state income tax, so you will never owe state taxes on any part of your settlement.

- Punitive damages, pre-judgment interest, and emotional distress damages not tied to a physical injury are taxable at the federal level.

- How your settlement is structured and allocated in the agreement directly affects your tax obligations.

- A qualified personal injury attorney can help you structure your settlement to minimize taxes legally.

Receiving a personal injury settlement can bring enormous relief after months of medical bills, lost paychecks, and pain. But once the settlement check arrives, many injury victims in Florida ask the same question: Do I have to pay taxes on this money?

Contact Injury LawStars today for a free case review or call (407) 887-4690 to discuss your personal injury claim with an experienced Florida attorney.

The short answer is that most personal injury settlements are not taxable, but certain portions can be. Understanding the difference between taxable and non-taxable settlement components can save you thousands of dollars and prevent an unwelcome surprise from the IRS.

This guide breaks down exactly which parts of a Florida personal injury settlement are taxable, which are tax-free, and what steps you can take to protect your compensation.

What Makes Personal Injury Settlements Different From Other Income?

Under normal circumstances, the IRS considers virtually all income taxable. Wages, investment returns, freelance income, and even prizes are all subject to federal income tax. So why are personal injury settlements treated differently?

The answer lies in the purpose of the payment. A personal injury settlement is designed to make you whole after someone else’s negligence caused you harm. It replaces what you lost, whether that means covering medical expenses, compensating for physical pain, or restoring income you could not earn while recovering. Congress recognized that taxing money meant to restore an injured person to their pre-accident condition would be unfair, which is why specific tax exclusions exist.

However, not every dollar in a settlement serves a purely compensatory purpose. Some components, like punitive damages or interest on delayed payments, go beyond restoring what was lost. The IRS treats these differently, and understanding where the line falls is critical for anyone receiving a personal injury settlement in Florida.

How Does IRS Section 104(a)(2) Protect Your Settlement?

The federal tax code provision that governs personal injury settlement taxation is Internal Revenue Code Section 104(a)(2). This section states that damages received “on account of personal physical injuries or physical sickness” are excluded from gross income. This exclusion applies whether you receive the money through a court judgment or a negotiated settlement, and whether it arrives as a lump sum or periodic payments.

For the exclusion to apply, two conditions must be met:

- The claim must involve a physical injury or physical sickness. Purely emotional or psychological claims without a physical component do not qualify for the exclusion.

- The damages must be compensatory, not punitive. Section 104(a)(2) specifically excludes punitive damages from the tax exemption.

This means that if you were injured in a car accident, truck accident, slip and fall, or any other incident that caused physical harm, the compensation you receive for that physical injury is generally tax-free at the federal level.

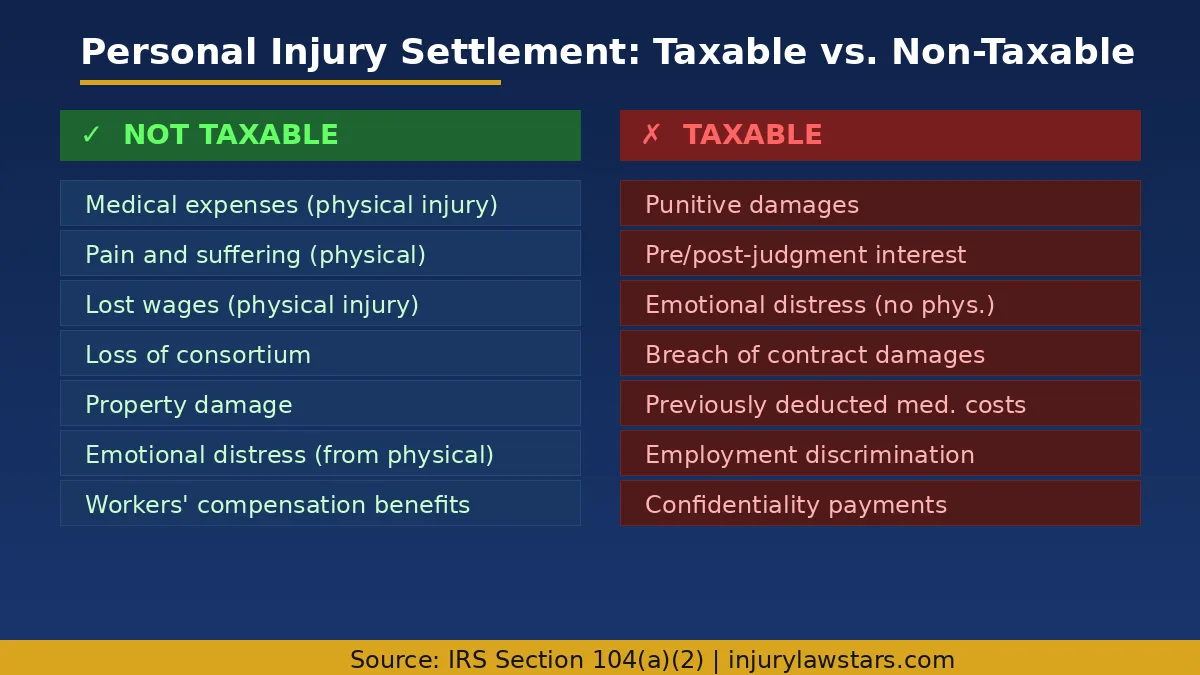

What Parts of a Personal Injury Settlement Are Not Taxable?

The following categories of damages are typically excluded from federal income tax when they stem from a physical injury or physical sickness:

Medical Expenses

Compensation for past and future medical bills related to your physical injury is not taxable. This includes emergency room visits, surgeries, physical therapy, prescription medications, rehabilitation, and any ongoing medical care tied to your injuries. However, there is one important exception: if you previously deducted medical expenses on your tax return and then receive settlement money reimbursing those same expenses, you may need to report that reimbursed amount as income. This is known as the medical expense deduction recapture rule.

Pain and Suffering

Compensation for pain and suffering connected to a physical injury is not taxable. This covers both the physical discomfort and the emotional distress that results directly from your physical injuries. The key requirement is that the pain and suffering must be linked to a physical injury, not a standalone emotional claim.

Lost Wages Tied to Physical Injury

When lost wages are included as part of a physical injury settlement, they are generally not taxable under Section 104(a)(2). This may seem counterintuitive since wages are normally taxable income, but the IRS recognizes that lost wage compensation in a physical injury case is fundamentally different from employment income. It replaces earnings you could not make because of your physical injuries.

Loss of Consortium

Damages paid to a spouse for loss of companionship, affection, or marital relations caused by the injured person’s physical injuries are generally not taxable, provided they originate from a physical injury claim.

Property Damage

Compensation for damaged or destroyed property, such as vehicle repair or replacement costs after a car accident, is generally not taxable as long as the payment does not exceed the property’s adjusted basis (essentially, what you paid for it). If the settlement exceeds the adjusted basis, the excess may be considered taxable gain.

What Parts of a Personal Injury Settlement Are Taxable?

While the majority of a physical injury settlement is typically tax-free, several categories of damages are subject to federal income tax regardless of whether the underlying case involves a physical injury:

Are Punitive Damages Taxable?

Yes. Punitive damages are always taxable under federal law. Unlike compensatory damages that reimburse your losses, punitive damages are awarded to punish the defendant for egregious behavior. Because they are not compensating you for a loss, the IRS treats them as taxable income. This applies even when punitive damages are awarded alongside a physical injury claim.

There is one narrow exception: in states where the wrongful death statute allows only punitive damages, those damages may be excluded. Florida’s wrongful death law allows compensatory damages, so this exception generally does not apply in Florida cases.

Is Interest on a Settlement Taxable?

Yes. Pre-judgment and post-judgment interest added to your settlement or court award is taxable income. Interest accrues when there is a delay between the injury and the payment, and the IRS considers this interest income regardless of the underlying claim type.

Emotional Distress Not Tied to Physical Injury

If you receive compensation for emotional distress that does not originate from a physical injury or physical sickness, that amount is taxable. For example, if you filed a claim for workplace harassment that caused anxiety and depression but no physical injury, the damages for emotional distress would be subject to federal income tax. However, you can reduce the taxable amount by the cost of medical treatment for the emotional distress (such as therapy or counseling costs).

Breach of Contract and Other Non-Physical Claims

Settlements for breach of contract, employment discrimination (without physical injury), defamation, or other non-physical injury claims are generally taxable because they do not fall under the Section 104(a)(2) exclusion.

How Does Florida’s Lack of State Income Tax Affect Your Settlement?

Florida is one of the few states in the country that does not impose a personal income tax. This provides a significant advantage for personal injury settlement recipients compared to residents of states like California, New York, or Illinois where state income tax rates can reach 10% or higher.

Here is what Florida’s tax structure means for your settlement:

- No state taxes on any part of your settlement. Whether your settlement includes compensatory damages, punitive damages, or interest, Florida will not tax any portion at the state level.

- Federal tax rules still apply. Even though Florida does not impose state income tax, you must still follow IRS rules for reporting and paying federal taxes on taxable settlement components.

- Potential savings on taxable components. If your settlement includes punitive damages or interest, you will only owe federal income tax on those amounts. In a state with income tax, you would owe both federal and state taxes, making Florida a more favorable place to receive a settlement.

If you have been injured in Florida and need help maximizing your settlement, reach out to Injury LawStars or call (407) 887-4690 for a free consultation.

How Can You Avoid Paying Taxes on Settlement Money?

While you cannot entirely eliminate federal taxes on inherently taxable settlement components, there are several legal strategies that can help minimize your tax burden:

Proper Settlement Allocation

How your settlement is allocated in the settlement agreement matters enormously. The agreement should clearly specify which portions compensate for physical injuries, medical expenses, lost wages tied to physical injury, pain and suffering, and other categories. Vague or improperly allocated settlements can lead to the IRS treating ambiguous amounts as taxable income. Work with your attorney to ensure the settlement language precisely reflects the nature of each payment.

Structured Settlements

A structured settlement spreads your compensation over time through periodic payments rather than a single lump sum. Structured settlements can offer significant tax advantages:

- The full amount, including any growth or interest earned within the structured settlement, remains tax-free if the underlying damages are for physical injury.

- Periodic payments can help you manage your finances over time and avoid spending a large lump sum too quickly.

- Investment gains within a structured settlement are not taxed, unlike gains you might earn if you invested a lump sum on your own.

Structured settlements are especially valuable for large settlements or for individuals who want guaranteed, long-term income.

Separate Physical and Non-Physical Claims

If your case involves both physical injury claims and non-physical claims (such as a separate breach of contract or employment dispute), your attorney can negotiate to allocate more of the settlement toward the physical injury components, which are tax-free. This must be done honestly and reflect the actual nature of the damages, but proper allocation is a legitimate and commonly used strategy.

Document Everything

Keep thorough records of all medical treatments, out-of-pocket expenses, and communications related to your injury. Strong documentation supports the categorization of your settlement as compensation for physical injuries and helps defend the tax-free treatment of your settlement if the IRS ever questions it.

Do You Need to Report Your Settlement to the IRS?

Even if your entire settlement is non-taxable, you may still need to be aware of IRS reporting requirements:

- Form 1099-MISC: If the payer (typically the insurance company or defendant) considers any portion of your settlement taxable, they may issue a Form 1099-MISC reporting the payment. You will need to address this on your tax return, even if you believe the amount is excludable under Section 104(a)(2).

- No 1099 for non-taxable amounts: If your entire settlement is for physical injuries and is non-taxable, the payer generally will not issue a 1099. However, it is wise to keep your settlement agreement and attorney correspondence as documentation.

- Attorney fees: If you paid your attorney on a contingency fee basis (which is standard in personal injury cases), the tax treatment of attorney fees depends on the underlying claim. For physical injury settlements excluded under Section 104(a)(2), the attorney’s share is typically not reported as your income.

What Common Tax Mistakes Should You Avoid With Your Settlement?

Settlement recipients frequently make errors that create unnecessary tax liability. Here are the most common mistakes to avoid:

- Failing to allocate the settlement properly. If your settlement agreement does not specify what each payment covers, the IRS may treat the entire amount as taxable. Always insist on clear allocation language.

- Forgetting about the medical expense deduction recapture. If you deducted medical expenses in a prior year and your settlement reimburses those same expenses, you must report the reimbursed amount as income.

- Ignoring interest. Interest on a settlement is taxable even when the underlying damages are not. Many recipients overlook interest income and fail to report it.

- Not consulting a tax professional. Personal injury settlement taxation can be complex, especially when your settlement includes multiple damage categories. A tax advisor who understands settlement taxation can help you plan effectively and avoid costly mistakes.

- Spending the settlement without reserving funds for taxes. If any portion of your settlement is taxable, set aside enough to cover the federal tax liability before spending the rest. Failing to do so can result in penalties and interest from the IRS.

When Should You Consult a Tax Professional About Your Settlement?

While many straightforward physical injury settlements do not require specialized tax advice, you should consult a tax professional or CPA if:

- Your settlement includes punitive damages or interest.

- Your settlement involves both physical and non-physical injury claims.

- You previously deducted medical expenses that your settlement now reimburses.

- Your settlement is large enough to significantly affect your overall tax bracket.

- You are considering a structured settlement and want to understand the long-term tax implications.

- You received a Form 1099-MISC for amounts you believe are non-taxable.

A qualified tax professional can help ensure you comply with federal requirements while keeping as much of your settlement as possible.

Need an experienced Florida personal injury attorney who understands how to protect your settlement? Contact Injury LawStars or call (407) 887-4690 for a free consultation today.

Frequently Asked Questions About Personal Injury Settlement Taxes

Are personal injury settlements taxable in Florida?

Most personal injury settlements for physical injuries are not taxable at the federal level under IRS Section 104(a)(2), and Florida has no state income tax. However, punitive damages, pre-judgment interest, and emotional distress damages not connected to a physical injury are taxable under federal law.

Do you have to pay taxes on a settlement for a car accident?

Generally no, if the settlement compensates you for physical injuries from the car accident. Compensation for medical bills, pain and suffering, and lost wages tied to your physical injuries is typically tax-free. Punitive damages or interest would be taxable.

How can I avoid paying taxes on settlement money?

Ensure your settlement agreement clearly allocates payments to physical injury categories, consider a structured settlement for large awards, keep detailed documentation of your injuries and medical treatment, and work with both a personal injury attorney and a tax professional to structure your settlement favorably.

Are lost wages from a personal injury settlement taxable?

Lost wages included in a physical injury settlement are generally not taxable under Section 104(a)(2). However, if the lost wages are part of a non-physical injury claim (such as employment discrimination without physical injury), they would be taxable.

Is workers’ compensation taxable in Florida?

No. Workers’ compensation benefits are generally not taxable at either the federal or state level, provided you do not also receive Social Security disability benefits. If you receive both, a portion of your workers’ compensation may become taxable.

What happens if I get a 1099 for my settlement?

If you receive a Form 1099-MISC, you should report it on your tax return but may be able to exclude the amount from taxable income if the settlement qualifies under Section 104(a)(2). Consult a tax professional to properly handle the reporting and claim the exclusion.