March 24, 2026

Florida No-Fault Insurance and PIP Explained: What Injury Victims Need to Know

Key Takeaway: Florida is a no-fault insurance state, which means your own Personal Injury Protection (PIP) policy pays for your medical bills and lost wages after a car accident, regardless of who caused the crash. But PIP only covers up to $10,000, pays just 80% of medical costs and 60% of lost wages, and requires you to seek treatment within 14 days. When your injuries are serious, you can step outside the no-fault system and pursue a claim against the at-fault driver. Understanding how Florida no-fault insurance works is critical to protecting your rights and getting the compensation you deserve.

If you have been injured in a car accident in Florida, you have probably heard terms like “no-fault insurance,” “PIP coverage,” and “personal injury protection” thrown around by insurance adjusters, doctors, and well-meaning friends. But what do these terms actually mean for you and your recovery?

Contact Injury LawStars today for a free case review at (407) 887-4690. No fees unless we win.

Florida’s no-fault insurance system is designed to get medical bills paid quickly after a crash, but it comes with strict rules, tight deadlines, and significant coverage limitations that catch most accident victims off guard. The $10,000 PIP limit sounds reassuring until you realize that a single emergency room visit can exceed that amount.

As a Florida car accident lawyer who has represented hundreds of injury victims across Clermont, Ocala, The Villages, and communities throughout Central Florida, Attorney Katie Miller knows firsthand how confusing this system can be. She was once an injury victim herself and understands the fear, stress, and frustration you face when dealing with insurance companies after an accident.

This guide breaks down everything you need to know about Florida no-fault insurance and PIP coverage, including what it covers, what it does not cover, critical deadlines you cannot miss, and when you have the right to pursue additional compensation beyond your PIP benefits.

What Is No-Fault Insurance in Florida?

Florida is one of approximately 12 states that operate under a no-fault auto insurance system. The no-fault system has been in place since 1971, and it fundamentally changes how medical expenses and lost wages are handled after a motor vehicle accident.

In a no-fault state like Florida, each driver’s own insurance policy pays for their injuries after a crash, regardless of who caused the accident. This is the opposite of what happens in a traditional “tort” or “at-fault” state, where the driver who caused the accident is responsible for paying the injured person’s medical bills and other damages.

The no-fault system is governed by the Florida Motor Vehicle No-Fault Law, codified under Florida Statute §627.736. The primary goal was to reduce the number of lawsuits clogging Florida’s court system by having each driver’s insurance handle their own medical expenses up to a certain limit.

How No-Fault Works in Practice

Here is a simplified example of how Florida no-fault insurance works after a car accident:

- You are involved in a car accident in Clermont, Lake County.

- Regardless of who caused the crash, you file a claim with your own auto insurance company.

- Your PIP coverage pays for up to $10,000 in medical expenses and lost wages.

- The other driver files a claim with their own insurance company for their injuries.

- Neither driver sues the other unless injuries meet the “serious injury threshold” (more on that below).

This system means that even if the other driver ran a red light and hit you, you still go to your own insurance company first. Many accident victims find this counterintuitive and frustrating, especially when they did nothing wrong.

No-Fault vs. At-Fault: Understanding the Difference

| Feature | Florida No-Fault System | Traditional At-Fault System |

|---|---|---|

| Who pays for your medical bills | Your own insurance (PIP) | The at-fault driver’s insurance |

| Fault determination required | Not for initial benefits | Yes, before any payment |

| Speed of payment | Faster (your own insurer pays) | Slower (requires fault investigation) |

| Right to sue | Limited by serious injury threshold | Generally unrestricted |

| Pain and suffering recovery | Only if injuries meet threshold | Available in most cases |

| Property damage | At-fault driver’s insurance pays | At-fault driver’s insurance pays |

One important distinction: while the no-fault system applies to medical expenses and lost wages, property damage in Florida still follows the at-fault system. The driver who caused the crash is responsible for paying for damage to your vehicle through their Property Damage Liability (PDL) coverage.

What Is PIP Insurance in Florida?

Personal Injury Protection, commonly known as PIP, is the insurance coverage that makes Florida’s no-fault system work. Every driver who registers a motor vehicle with four or more wheels in Florida is required by law to carry a minimum of $10,000 in PIP coverage and $10,000 in Property Damage Liability (PDL) coverage. This is often referred to as Florida’s “10/10” minimum coverage requirement.

PIP is unique because it pays benefits to the policyholder regardless of who was at fault in the accident. It is designed to provide quick access to funds for medical treatment and wage replacement so that accident victims can begin recovering without waiting months or years for a fault determination.

What PIP Covers

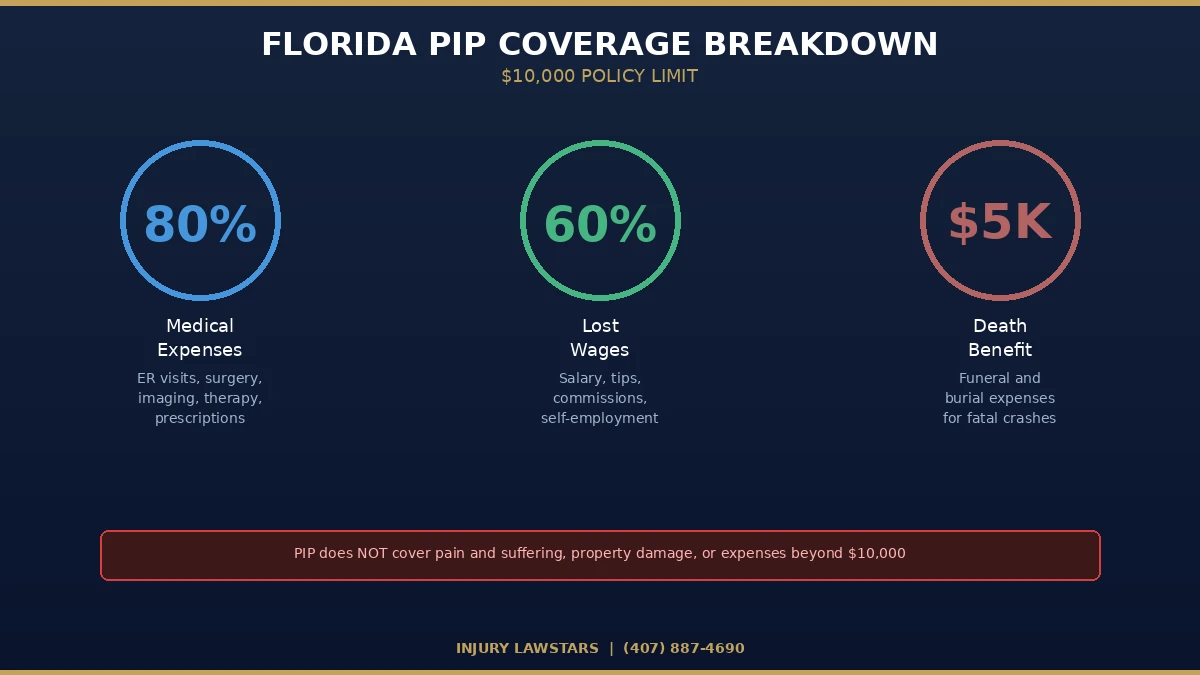

Under Florida law, PIP coverage provides the following benefits up to your policy limit (minimum $10,000):

Medical Expenses (80% Coverage)

PIP pays 80% of all reasonable, related, and necessary medical expenses resulting from a covered accident. This includes:

- Emergency room visits and hospital stays

- Doctor visits and specialist consultations

- Diagnostic imaging (X-rays, MRIs, CT scans)

- Surgery and surgical procedures

- Prescription medications

- Physical therapy and rehabilitation

- Chiropractic treatment

- Dental treatment for injuries sustained in the crash

Lost Wages (60% Coverage)

If your injuries prevent you from working, PIP pays 60% of your lost income, subject to the overall policy limit. This applies to wages, salary, tips, commissions, and other forms of earned income.

Replacement Services (60% Coverage)

PIP may also cover 60% of expenses for services you normally performed yourself but cannot do because of your injuries, such as household chores, childcare, or yard maintenance.

Death Benefits ($5,000)

If a covered accident results in death, PIP provides a $5,000 benefit to the deceased person’s estate for funeral and burial expenses.

What PIP Does NOT Cover

Understanding what PIP does not cover is just as important as knowing what it does:

- Pain and suffering – PIP does not compensate you for physical pain, emotional distress, or mental anguish

- Full wage replacement – PIP only covers 60% of lost income, leaving you responsible for the remaining 40%

- Expenses beyond $10,000 – Once you hit the policy limit, PIP coverage ends

- Property damage – Your vehicle damage is not covered by PIP

- Long-term disability – PIP does not cover ongoing disability beyond the policy limits

- Non-economic damages – Loss of enjoyment of life, loss of consortium, and similar damages are not covered

- Injuries unrelated to the accident – Pre-existing conditions not aggravated by the crash are excluded

The gap between what PIP covers and what accident victims actually need is often enormous. A serious car accident on Interstate 4, the Florida Turnpike, or US Route 27 in Lake County can result in medical bills that reach $50,000, $100,000, or more. PIP’s $10,000 limit barely scratches the surface.

The $10,000 PIP Limit: Why It Falls Short

The $10,000 PIP limit has not changed since the no-fault law was enacted in 1971. While medical costs have skyrocketed over the past five decades, this coverage cap has remained frozen.

Consider these common costs for car accident injuries:

- Emergency room visit: $2,000 to $5,000 or more

- Ambulance transport: $500 to $2,500

- MRI scan: $1,000 to $3,000

- Broken bone treatment: $5,000 to $15,000

- Surgery: $10,000 to $100,000+

- Physical therapy (per session): $75 to $350

- Traumatic brain injury treatment: $85,000 to $3 million (over a lifetime)

A single emergency room visit following a moderate car accident can eat through half or more of your PIP coverage. If you need surgery, diagnostic imaging, and follow-up care, you will almost certainly exceed the $10,000 limit within weeks.

This is why understanding your rights beyond PIP is essential. When your injuries are serious, Florida law allows you to step outside the no-fault system and pursue a claim against the at-fault driver for your full damages, including pain and suffering. An experienced car accident attorney can help you determine whether your injuries qualify.

The 14-Day Rule: A Deadline You Cannot Miss

One of the most critical and least understood aspects of Florida PIP insurance is the 14-day rule. Under Florida Statute §627.736, you must seek initial medical treatment within 14 days of the accident to qualify for PIP benefits.

Day 1 is the date of the accident. Day 14 is your absolute deadline.

If you fail to see a doctor, visit an emergency room, or receive treatment from a qualified medical provider within this 14-day window, your PIP benefits can be denied entirely. It does not matter how severe your injuries are or how clear the connection between the accident and your symptoms may be.

Why the 14-Day Rule Matters

Many accident victims make the mistake of “waiting to see if it gets better.” Adrenaline can mask pain for hours or even days after a crash. Soft tissue injuries like whiplash, herniated discs, and internal bleeding may not produce noticeable symptoms immediately.

Here is what can happen if you wait:

- Day 1-3: You feel sore but assume it is nothing serious

- Day 7: Pain worsens, you consider seeing a doctor

- Day 14: Your symptoms become severe

- Day 15: You finally go to the emergency room, but your PIP benefits are now at risk

The insurance company does not care about the reason for the delay. If you did not receive qualifying medical care within 14 days, they have a legal basis to deny your claim.

Who Qualifies as a Medical Provider Under the 14-Day Rule

Not every healthcare provider counts for satisfying the 14-day requirement. Florida law specifies the following qualifying providers:

- Licensed medical doctors (MDs)

- Licensed osteopathic physicians (DOs)

- Licensed dentists (for dental injuries)

- Licensed physician assistants

- Licensed advanced practice registered nurses

- Emergency room physicians and staff

- Licensed hospitals and emergency departments

Chiropractors and physical therapists may provide treatment, but they may not satisfy the initial 14-day requirement unless they can document an Emergency Medical Condition (EMC).

The Emergency Medical Condition (EMC) Requirement

Florida PIP coverage includes a critical distinction based on the severity of your injuries:

- With an EMC diagnosis: You qualify for the full $10,000 in PIP benefits

- Without an EMC diagnosis: Your PIP benefits are capped at just $2,500

An Emergency Medical Condition is defined under Florida law as a medical condition that manifests itself by acute symptoms of sufficient severity that the absence of immediate medical attention could reasonably be expected to result in serious jeopardy to patient health, serious impairment of bodily functions, or serious dysfunction of any bodily organ or part.

This means that if a doctor determines your injuries are relatively minor and do not constitute an EMC, your PIP coverage drops from $10,000 to just $2,500. That $2,500 may cover an emergency room visit and one follow-up appointment, leaving you responsible for the rest.

This is another reason why seeking immediate medical attention after any accident is so important. Early medical documentation establishes the severity of your injuries and supports an EMC determination, which directly affects how much PIP coverage you receive.

When You Can Step Outside the No-Fault System

Florida’s no-fault system is not absolute. The law provides a pathway for accident victims with serious injuries to step outside the no-fault system and file a lawsuit against the at-fault driver for full damages, including pain and suffering.

Under Florida Statute §627.737, you can pursue a claim against the at-fault driver if your injuries meet the “serious injury threshold.” This means your injuries must result in at least one of the following:

- Significant and permanent loss of an important bodily function

- Permanent injury within a reasonable degree of medical probability

- Significant and permanent scarring or disfigurement

- Death

What Qualifies as a Serious Injury

The serious injury threshold is intentionally broad enough to cover a wide range of severe injuries that accident victims in Florida commonly experience. Examples include:

- Traumatic brain injuries – Even a “mild” concussion can cause permanent cognitive impairment. If you have suffered a brain injury in a car accident, you likely meet the threshold.

- Spinal cord injuries and herniated discs – Injuries that cause chronic pain, limited mobility, or nerve damage often qualify as permanent impairment.

- Broken bones with lasting complications – Fractures that require surgical repair, hardware implantation, or result in reduced range of motion.

- Internal organ damage – Injuries to the liver, spleen, kidneys, or other organs that require emergency surgery.

- Amputation – Loss of any limb or digit.

- Severe burns and scarring – Burns, lacerations, or other injuries that result in permanent visible scarring.

- Wrongful death – When a car accident results in the death of a loved one, surviving family members can pursue a wrongful death claim.

Damages Available Outside No-Fault

When you step outside the no-fault system, you can pursue compensation for damages that PIP does not cover:

- All medical expenses (past and future, not limited to $10,000)

- All lost wages (100%, not limited to 60%)

- Loss of future earning capacity

- Pain and suffering

- Emotional distress

- Loss of enjoyment of life

- Loss of consortium (impact on your relationship with your spouse)

- Scarring and disfigurement

- Permanent disability

These damages can be significant. While PIP caps your benefits at $10,000, a personal injury claim for serious injuries can recover hundreds of thousands or even millions of dollars in compensation.

How No-Fault Insurance Affects Different Types of Accidents

Florida’s no-fault insurance system primarily applies to motor vehicle accidents, but the specifics vary depending on the type of accident involved.

Car Accidents

Car accidents are the most common type of claim under Florida’s no-fault system. Whether you are rear-ended on I-4 near Orlando, involved in a T-bone collision on US-441 through Lake County, or hit by a distracted driver on State Road 50 in Clermont, your PIP coverage is your first source of compensation for injuries.

If your injuries are serious, a Florida car accident lawyer can help you pursue a claim against the at-fault driver for full damages beyond PIP.

Truck Accidents

Accidents involving commercial trucks and tractor-trailers often result in catastrophic injuries due to the massive size and weight difference between commercial vehicles and passenger cars. While your own PIP coverage still applies, the severity of truck accident injuries frequently meets the serious injury threshold, allowing victims to pursue substantial claims against the trucking company and driver. An experienced truck accident lawyer understands the complex regulations governing commercial carriers.

Motorcycle Accidents

Here is an important exception: motorcycles are not covered by Florida’s PIP requirement. Florida Statute §627.736 applies to motor vehicles with four or more wheels. Motorcycle owners are not required to carry PIP coverage, which means riders do not have the same no-fault safety net after an accident.

If you are injured in a motorcycle accident, you may need to rely on your health insurance, uninsured/underinsured motorist coverage, or a personal injury claim against the at-fault driver. A motorcycle accident attorney can help you explore all available options for compensation.

Bicycle and Pedestrian Accidents

Bicyclists and pedestrians can be covered by PIP if they have their own auto insurance policy or live with a family member who does. If you are hit by a car while walking or cycling in Clermont, Ocala, or anywhere in Florida, you may be able to access PIP benefits through your household’s auto policy.

However, bicycle and pedestrian accidents frequently result in severe injuries because the victim has no protection from the force of impact. These injuries often exceed PIP limits and meet the serious injury threshold. A bicycle accident lawyer or attorney experienced in pedestrian accident claims can help you pursue full compensation.

Boating Accidents

Florida’s no-fault insurance and PIP requirements apply specifically to motor vehicles, not watercraft. If you are injured in a boating accident on one of Florida’s lakes, rivers, or coastal waterways, PIP coverage does not apply. Instead, you would need to pursue a claim through the boat operator’s liability insurance or through a personal injury lawsuit.

Drunk Driving Accidents

When you are hit by a drunk driver, your PIP coverage still pays first for your initial medical expenses and lost wages. But drunk driving accidents frequently cause severe or fatal injuries that far exceed PIP limits. Additionally, if the drunk driver’s actions were particularly reckless, you may be entitled to punitive damages, which are designed to punish the wrongdoer and deter similar behavior. A drunk driving accident lawyer can help you pursue maximum compensation.

Common Misconceptions About Florida No-Fault Insurance

Florida’s no-fault system is widely misunderstood. Here are the most common misconceptions that can cost accident victims thousands of dollars:

Misconception #1: “No-Fault Means Nobody Is at Fault”

This is the most common misunderstanding. “No-fault” does not mean that no one is responsible for the accident. It simply means that, initially, each driver’s own insurance pays for their medical expenses regardless of who caused the crash. Fault still matters when injuries are serious enough to step outside the no-fault system.

Misconception #2: “PIP Covers All of My Medical Bills”

PIP covers only 80% of medical expenses up to the $10,000 policy limit. That means you are responsible for the remaining 20%, and once the $10,000 cap is reached, PIP pays nothing further. Many accident victims are shocked to discover that PIP runs out after just a few doctor visits and one or two imaging studies.

Misconception #3: “I Cannot Sue the Other Driver in Florida”

You absolutely can sue the other driver in Florida if your injuries meet the serious injury threshold. The no-fault system only restricts lawsuits for minor injuries. If you have suffered a significant and permanent injury, you retain the full right to pursue compensation from the at-fault driver.

Misconception #4: “I Have Plenty of Time to See a Doctor”

The 14-day rule is absolute. Many accident victims lose their PIP benefits entirely because they waited too long to seek medical treatment. Even if your symptoms seem minor immediately after the crash, see a doctor within 14 days. Delayed symptoms are common in car accidents, particularly for soft tissue injuries, concussions, and internal injuries.

Misconception #5: “My Health Insurance Will Cover Everything PIP Doesn’t”

While your health insurance may pick up some costs after PIP is exhausted, health insurance policies have their own deductibles, copays, and coverage limitations. Additionally, your health insurance company may assert a subrogation lien, meaning they can demand repayment from any personal injury settlement you receive. Navigating the interaction between PIP and health insurance requires careful planning.

Misconception #6: “No-Fault Insurance Means I Do Not Need a Lawyer”

This may be the most costly misconception of all. Insurance companies have teams of adjusters and attorneys working to minimize what they pay on every claim. Having a personal injury attorney on your side ensures that your PIP claim is handled correctly, that the 14-day rule and EMC requirements are satisfied, and that you are aware of your right to pursue additional compensation when your injuries are serious.

Injured in a car accident? Call Injury LawStars at (407) 887-4690 for a free consultation.

2026 Legislative Update: The Future of Florida PIP

Florida’s no-fault insurance system may be facing its biggest change in over 50 years. Legislation has been introduced that would repeal mandatory PIP coverage effective July 1, 2026, replacing it with a new insurance framework.

What the Proposed Changes Include

Under the proposed legislation, Florida would transition from its current no-fault system to a fault-based system with the following requirements:

- Mandatory Bodily Injury Liability (BIL): $25,000 per person and $50,000 per accident

- Mandatory Medical Payments Coverage (MedPay): $5,000

- Elimination of PIP: The $10,000 PIP requirement would be removed

What This Means for Florida Drivers

If the PIP repeal takes effect, the changes would fundamentally alter how accident claims work in Florida:

- Fault would matter from the start: Instead of filing a claim with your own insurer, the at-fault driver’s insurance would be responsible for paying your medical bills

- Higher minimum coverage: The $25,000/$50,000 BIL requirement provides more coverage than the current $10,000 PIP minimum

- MedPay replaces PIP: The $5,000 MedPay coverage is lower than the current $10,000 PIP but works differently

- No 14-day rule: The strict 14-day treatment deadline would no longer apply under MedPay

- Potential premium impacts: Some drivers may see premium changes as the insurance market adjusts

What You Should Do Right Now

Regardless of whether the PIP repeal passes, the current rules remain in effect until the effective date of any new legislation. If you are injured in a car accident today, the no-fault system and PIP requirements described in this article apply.

Attorney Katie Miller and the team at Injury LawStars are closely monitoring these legislative developments. Whether the law changes or not, our commitment to fighting for injured people throughout Florida remains the same.

Why You Need an Attorney for Your PIP Claim

Insurance companies are in the business of collecting premiums and paying out as little as possible. When you file a PIP claim, you are dealing with adjusters who are trained to find reasons to reduce or deny your benefits.

Here is how a personal injury attorney can help:

Protecting Your PIP Benefits

- Ensuring the 14-day rule is met by connecting you with qualified medical providers immediately

- Documenting your EMC to secure the full $10,000 in PIP benefits rather than the $2,500 non-EMC limit

- Challenging improper PIP denials when your insurance company refuses to pay legitimate claims

- Coordinating with your medical providers to ensure proper billing and documentation

Pursuing Compensation Beyond PIP

- Evaluating whether your injuries meet the serious injury threshold to step outside no-fault

- Filing a personal injury claim against the at-fault driver for full damages

- Negotiating with insurance companies to maximize your settlement

- Taking your case to trial if the insurance company refuses to offer fair compensation

The Injury LawStars Difference

Attorney Katie Miller was once an injury victim herself. She knows what it feels like to be overwhelmed, in pain, and unsure who to trust. That firsthand experience drives her relentless advocacy for every client at Injury LawStars.

Injury LawStars serves injured clients throughout Florida, including Clermont, Eustis, Leesburg, Mount Dora, Tavares, and surrounding Lake County communities, as well as Ocala, The Villages, Wildwood, Orlando, Tampa, Jacksonville, and across the state. Whether you were injured in a car accident, truck accident, motorcycle crash, or any other type of accident, we are here to fight for you.

We work on a contingency fee basis, which means you pay nothing unless we win your case. There is no risk to you for getting the legal help you need.

Frequently Asked Questions About Florida No-Fault Insurance

Is Florida a no-fault state for car insurance?

Yes. Florida has been a no-fault state since 1971. Under the Florida Motor Vehicle No-Fault Law (Florida Statute §627.736), all drivers are required to carry Personal Injury Protection (PIP) insurance. After a car accident, you file a claim with your own insurance company for medical expenses and lost wages, regardless of who was at fault.

What does PIP cover in Florida?

PIP covers 80% of reasonable and necessary medical expenses, 60% of lost wages if you cannot work due to your injuries, 60% of replacement services for tasks you can no longer perform, and a $5,000 death benefit. The minimum coverage limit is $10,000.

What is the 14-day rule for PIP in Florida?

Florida law requires you to seek medical treatment within 14 days of a motor vehicle accident to qualify for PIP benefits. If you do not receive qualifying medical care within this window, your insurance company can deny your PIP claim entirely. This deadline applies regardless of the severity of your injuries.

Can I sue the other driver in Florida if it was their fault?

Yes, but only if your injuries meet the “serious injury threshold.” This means your injuries must result in significant and permanent loss of an important bodily function, permanent injury, significant and permanent scarring or disfigurement, or death. If your injuries meet this threshold, you can step outside the no-fault system and pursue a claim for full damages, including pain and suffering.

What is the difference between an EMC and a non-EMC under PIP?

An Emergency Medical Condition (EMC) is a medical condition that requires immediate attention to prevent serious health consequences. If a doctor determines you have an EMC, you qualify for the full $10,000 in PIP benefits. Without an EMC diagnosis, your PIP benefits are limited to just $2,500. This distinction makes early, thorough medical documentation essential.

Does PIP cover motorcycle accidents?

No. Florida’s PIP requirement applies to motor vehicles with four or more wheels. Motorcycles are exempt from PIP coverage requirements. If you are injured in a motorcycle accident, you may need to rely on health insurance, uninsured/underinsured motorist coverage, or a personal injury claim against the at-fault driver. Contact a motorcycle accident attorney for guidance.

What happens when my PIP benefits run out?

When your $10,000 PIP limit is exhausted, your health insurance may cover additional medical expenses, subject to its own deductibles and limitations. If your injuries are serious enough to meet the serious injury threshold, you can pursue a personal injury claim against the at-fault driver for all damages beyond PIP, including medical bills, lost wages, and pain and suffering.

Is PIP being repealed in Florida?

Legislation has been proposed to repeal Florida’s PIP requirement effective July 1, 2026, replacing it with mandatory Bodily Injury Liability coverage ($25,000/$50,000) and $5,000 in Medical Payments (MedPay) coverage. Until any new law takes effect, the current PIP requirements remain in place.

How can a lawyer help with my PIP claim?

A personal injury attorney can ensure you meet the 14-day treatment deadline, help document your Emergency Medical Condition for full benefits, challenge wrongful PIP denials, coordinate with medical providers, and evaluate whether your injuries qualify for a claim beyond PIP against the at-fault driver. At Injury LawStars, we handle all of this at no upfront cost to you.

What should I do immediately after a car accident in Florida?

Seek medical attention within 14 days (ideally immediately), report the accident to your insurance company, document everything (photos, witness information, police report), keep all medical records and bills, and contact a personal injury attorney before accepting any settlement offer from the insurance company. The sooner you act, the better protected your rights will be.

This article is for informational purposes only and does not constitute legal advice. Every case is different. If you have been injured in an accident in Florida, contact Injury LawStars for a free consultation to discuss your specific situation. Attorney Katie Miller and our team are ready to fight for the compensation you deserve.

Call Injury LawStars today at (407) 887-4690 for a free case review. No fees unless we win.